When Float Changed for Berkshire Hathaway

Berkshire Hathaway's 1976 Annual Report

Note: This is basically the transcript of what I put out on The 10-K Podcast.

Something came to mind when studying Teledyne’s insurance companies, and I realized I needed to find answers.

When was Berkshire Hathaway first able to use its insurance float to buy stocks?

I realized that I got this wrong in the past. In my book on Berkshire, I didn’t really answer this question. It would have made for a good chapter in the book, but I was a little unsure about the answer at the time. There was a little bit of cowardice there, and my confusion should have been an important sign for me to dig in deeper on that topic. Anyways, more than 3 years after publishing the book, I am diving back into the topic. Also, in interviews I’ve given on podcasts, I’ve mentioned that Berkshire started investing its insurance float into stocks sometime around the 1990’s. I was wrong about that. I was viewing this question from the parent company perspective, when I should have been diving into the financials of just the Berkshire Hathaway Insurance Group, which is disclosed in the notes of Berkshire’s 10-K’s in most years. My focus in this article will mostly be around the Berkshire Hathaway Insurance Group itself, without mixing in equity capital invested in subsidiaries like the Illinois National Bank or the original textile operation.

Before going any further, let me give some background on the insurance business. The assets of an insurance company are funded with liabilities from policyholders’ funds, as well as from equity capital from shareholders’ funds. Policyholders’ funds are sometimes referred to as float, and those generally are invested into bonds or left in cash at most firms. The equity capital can be invested in stocks, but many insurance companies still invest a portion of their equity capital into bonds as well.

When Berkshire first got into the insurance business by acquiring National Indemnity, its balance sheet was structured just like this. Even before Berkshire got involved, National Indemnity was structured just about like I described. You can see financials for National Indemnity in Moody’s Manuals from that time period even before Berkshire acquired it. Today, National Indemnity is the organization that owns the Burlington Northern Santa Fe railroad. Even though BNSF is privately owned by Berkshire, it still files 10-K’s with the SEC. I believe this is due to its debt. If you open up the most recent 10-K, you can see on the first page that it says:

How did National Indemnity go from being restricted in how much it could invest in stocks, to owning an illiquid, massive railroad?

Let’s jump back to 1967, which was the year Berkshire acquired National Indemnity. The balance sheet for the National Indemnity Company is disclosed within Berkshire’s 10-K. The insurance subsidiary reported $6.4 million of stocks at fiscal year end, while it had $7.6 million of equity capital. Since its portfolio of stocks is less than its equity capital, this tells me that no liabilities funded the purchase of stocks. The firm had $21.8 million of bonds, as this is what National Indemnity invested its float into.

As you move through the 10-K’s of Berkshire for just about the next decade, the story remains the same. Equity capital for the insurance subsidiary exceeded the level of stocks on the balance sheet. This even became more pronounced after a handful of years. In 1971, the portfolio of stocks within the Berkshire Hathaway Insurance Group was less than half of its equity capital. It had equity capital of $35.2 million, while there were just $16.8 million of stocks on the balance sheet. At first glance, it’s almost like Berkshire was getting less aggressive investing in stocks once Warren Buffett took over. Why was this? I have my theories, but let me get back to that in a minute.

1976 is when everything changed. This is where I draw the line of demarcation for its insurance subsidiaries. The level of stocks within the insurance group just narrowly squeaked ahead of its equity capital. The subsidiary had $93 million of stocks, while there was $88 million of equity capital. I interpret this as about $5 million of stocks were funded by insurance liabilities in the form of float. Stocks consistently outpaced equity capital in the insurance group after this point in time, so this was a turning point for the organization.

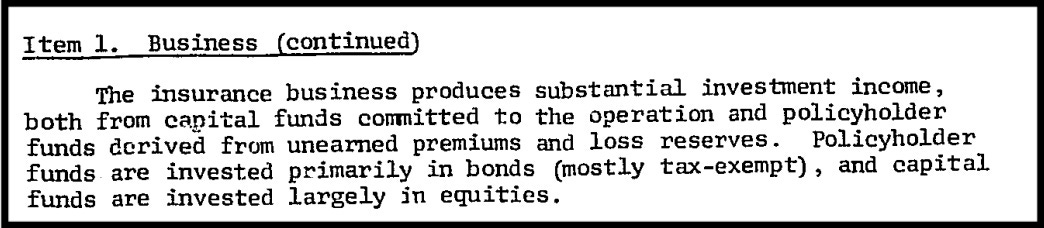

Below is an excerpt from Berkshire Hathaway’s 1976 Annual Report. This disclosure was common prior to 1976. Interestingly, I didn’t see this disclosure anytime after the 1976 report.

That last sentence is the key. “Policyholder funds are invested primarily in bonds, and capital funds are invested largely in equities”. What this is saying is that in 1976, and in the years leading up to this, insurance float was invested in bonds. If we take a look at the disclosure in 1977, the year that follows, the last sentence from that excerpt is taken out:

1976 is the first year that I see stocks exceed equity capital for the insurance group. The disclosure of float being invested in bonds was left in there in 1976, which makes sense to me given this was only the first year things started to change. The change was also somewhat small in 1976. By 1977, now Berkshire had two years in a row where stocks exceeded equity capital in the insurance group, so a trend was now forming. Float was being invested more aggressively. At this point, the disclosure I referred to was changed.

The aggressiveness of Berkshire’s investments accelerated as the years went on. In 1976, stocks were only 5% higher than equity capital in the insurance group. This trended higher over the years until stocks were more than 50% higher than equity capital in the insurance group in 1992. Instead of percentages, you could also look at dollar value. About $5 million of stocks were funded by float in 1976, while float funded $4.4 billion of stocks in 1992. Interestingly, stocks were only about 4% above equity capital in the year 2000. My assumption is that this was due to the skyrocketing valuations during the internet bubble of 1999 and 2000. Berkshire just had less investment opportunities in the stock market at that time.

What changed in 1976? My theory is that this relates to underwriting leverage. You could say that maybe stock market valuations played a role, or maybe it took nearly a decade for Buffett to plead his case to insurance regulators in the state of Nebraska. Both of those are possible answers. What really sticks out to me though is the story of underwriting leverage.

National Indemnity was fairly aggressive with its underwriting leverage under the previous ownership of Jack Ringwalt. The leverage wasn’t completely out of hand, but I get the sense that it was higher than someone like Buffett would be comfortable with. In a Moody’s Manual that I have, I see that National Indemnity wrote premiums of $12.7 million in 1964, while it had $4.6 million of equity capital at that time. This means you could say that sales were 2.76 times higher than capital. This is underwriting leverage, and it is one way to view risk at an insurance company.

One way to think about it is that each time an insurance company makes a sale, it is taking on risk because they might have to pay out claims on that insurance policy. Insurance companies then have some amount of equity capital to fall back on if there are losses on insurance policies. So a common way to look at risk and leverage in insurance is to compare revenue to capital, which in this case would be premiums written compared to statutory surplus or equity capital.

While 2.76 times leverage at National Indemnity wasn’t crazy, my guess is that this was just about as high as state regulators might allow for a small insurer like this. One benefit of Berkshire taking over was that it had additional equity capital invested outside of insurance. While National Indemnity’s capital level and leverage ratios might not have changed immediately at the subsidiary level, those did change if you view it from the parent company level.

In the initial years of Berkshire’s ownership, National Indemnity continued on with a similar level of underwriting leverage. My guess is that this was due to what Buffett viewed as an opportunity for growth. Insurance is a cyclical business, and it happened to be a good period for the industry. I mentioned that premiums written amounted to $12.7 million in 1964. Premiums written reached $66 million in 1971. This is some high growth. Berkshire took advantage of the opportunity to grow its insurance operation in the early years of its ownership. With all this growth in sales, it was hard for equity capital to keep up. This meant that it was hard to reduce underwriting leverage unless Berkshire wanted to slow down its growth. My theory is that this is why the balance sheet was more conservative in the early years of Berkshire owning National Indemnity. Since it had higher underwriting leverage than I assume Buffett would have wanted, it had its assets in safer bonds in the meantime. You only saw underwriting leverage like this from Berkshire in the early days when capital was limited. They were trying to diversify out of the original textile business, all while there happened to be an opportunity to grow in the insurance field. This opportunity is not always there, as Berkshire experienced plenty of periods of declining revenue in its insurance subsidiaries in later years.

By 1976, the year in which this all changed, underwriting leverage was down to a low level. At the subsidiary level, the insurance group had closer to 1 times leverage. It wrote premiums of $95 million, while it had equity capital of $88 million. Berkshire overall had $115 million of equity capital, as well as earnings coming in from industries outside of insurance. Once it had less leverage and more diversity, then you saw the balance sheet being invested more aggressively. I don’t think this is a coincidence. Underwriting leverage remained low for the rest of the story, all the way to the present day.

Now, back to some of the other theories that you could argue. The stock market went down in a major way in 1973 and 1974. By 1976, business results were improving, but the stock market was still at what most people might consider to be low, or at least reasonable, levels. In the last episode of The 10-K Podcast that I did on Teledyne, I mentioned that 1976 was the first year in which its insurance companies invested its insurance float into stocks. For Teledyne, I do think that this was a move to take advantage of the opportunity in the stock market. This was the only time period in which Teledyne invested its balance sheet this way. Prior to 1976, its float was invested into fixed income. By the mid 1980’s, it was back to being invested into fixed income. So for Teledyne, this looks like an opportunistic move. Berkshire got aggressively into stocks in 1976, and never changed its ways. The permanence of this move is why I think it was slightly less about stock market valuations. Low valuations certainly help make this possible, as Buffett almost ran out of ideas in 1999 and 2000, but I think this had less of an impact than underwriting leverage did.

The other theory I mentioned was related to insurance regulators. In the US, insurance is regulated at the state level. Nebraska is more lenient in how insurance companies invest in stocks than other states are. What came first - the chicken or the egg? Buffett is obviously from Nebraska, so maybe Berkshire had some influence there. But I’ve seen insurance companies reincorporate in other states. National Indemnity could have focused its business elsewhere if regulations forced it to. It is possible that it took nearly a decade for Buffett to convince regulators of investing insurance float into stocks. This could go hand in hand with underwriting leverage too, as regulators would be less likely to allow aggressiveness on the balance sheet if underwriting leverage was high. It took time for Berkshire to diversify itself out of textiles and out of insurance as well. So time could be one reason why it took until 1976 for the line of demarcation to occur. Again, this is certainly possible, but the main reason I go back to in my mind is underwriting leverage. That needed to be reduced before the float was invested more aggressively.

I mentioned that Teledyne invested its float into stocks in 1976. Although in this example Teledyne did have some underwriting leverage at the subsidiary level, it was conservative and diversified at the parent company level. Its Unicoa subsidiary had premiums earned of $263 million compared to equity capital of $135 million on a GAAP basis. This means that Unicoa nearly had twice the amount of revenue compared to its capital. Insurance was a much smaller part of the overall company for Teledyne though than it was for Berkshire. About 35% of Teledyne’s capital was invested in the insurance business, so I think it was pretty easy for Teledyne to get aggressive in 1976 when the opportunity presented itself.

At Berkshire, the story was pretty similar at the insurance group after 1976. There were a few years in the 1980’s where I didn’t see any disclosure of full financial statements for the Berkshire Hathaway Insurance Group - at least not in the versions of the annual reports that I had. The year 2000 was the last year in which I saw a full, separate breakout of financial statements for the insurance group as well. If you glance at the most recent 10-K, which was for 2022, there is a breakout on the balance sheet for “Insurance and Other”. I think this gets us close enough. There were $726 billion of assets reported in this section, which is just mind blowing. This is against $291 billion of liabilities. This leaves about $435 billion of equity capital in the “Insurance and Other” segment. There is also a line item for deferred taxes at the bottom of the balance sheet. Most of this is related to unrealized gains on stocks, so I think we could consider this in the calculation of insurance equity capital.

Berkshire only had $309 billion of stocks on the balance sheet, so obviously capital exceeded the level of stocks on the balance sheet either way. If you add the cash and treasury bills on the balance sheet with the amount of stocks Berkshire has, then you would get to the level of equity capital within the “Insurance and Other” segment. I interpret this as saying that Berkshire has none of its stocks currently funded by float. My guess is that this situation is due to a current lack of investment opportunities at the scale that Berkshire needs, not related to Berkshire’s inability to invest its float into stocks. Maybe I am misinterpreting the “Insurance and Other” segment of the balance sheet, and maybe “Other” includes unrelated businesses that make 2022 incomparable to the earlier decades. My feeling is that Berkshire’s ability to invest its float has only increased over time due to its size and its diversity in businesses.

Another interesting angle to explore is Buffett and Munger’s use of float at Blue Chip Stamps. This was a company that issued trading stamps that were involved in rewards programs for retailers. Blue Chip received cash upfront when they issued the stamps, and would incur costs later when customers redeemed stamps at retail outlets. This created a liability for unredeemed trading stamps on the balance sheet for Blue Chip, which was a form of float similar to insurance.

In certain ways, Blue Chip’s float was more valuable to Buffett and Munger than the insurance float was. The trading stamp industry was not heavily regulated like insurance, so they had much more flexibility in how they operated the business. Additionally, it was much easier to estimate future costs at Blue Chip than it would be at an insurance company. I don’t think there would be a big surprise in terms of how many trading stamps would be redeemed. You can have some large, unexpected catastrophes in the insurance business. Underwriting in the insurance business is the process of estimating your future costs. You are trying to make a very educated guess, but it’s still a guess. With that being said, the insurance industry ended up being much more stable over the very long term. The trading stamp industry disappeared, and this meant that Blue Chip’s original business eventually became extinct. Personally, I can’t imagine the insurance industry going extinct anytime soon. Buffett and Munger invested the float at Blue Chip so skillfully, and managed the company so well, that their investment still worked out beautifully. By the 1980’s though, the trading stamp revenue at Blue Chip declined by more than 90%, leaving the original business of Blue Chip just about finished.

At the end of the day, what did this look like in practice? Blue Chip had around $100 million of stocks on the balance sheet in 1972. Its equity capital was just $46 million. It is pretty incredible that Blue Chip had more than double the amount of stocks on the balance sheet than it had in entire equity capital. Berkshire’s insurance companies never invested this much float into stocks. This is why Blue Chip’s value survived even though its original business did not.

To close this out, I want to circle back to my previous mistake in thinking. I used to view Berkshire and its use of float from the parent company perspective. I would see how much equity capital Berkshire had overall compared to its portfolio of stocks. I don’t think this was very intelligent. It is much better to just view the financial statements of the Berkshire Hathaway Insurance Group, and strip out the noise from the unrelated businesses - at least for this exercise. Basically, when stocks exceed the equity capital invested into insurance, then stocks must be partially funded by float.

Thank you for letting me revisit Berkshire’s history once again. Warren Buffett and Charlie Munger seem to have created something that continues to look interesting the more angles you view it from.