The Coca-Cola Company in 1923

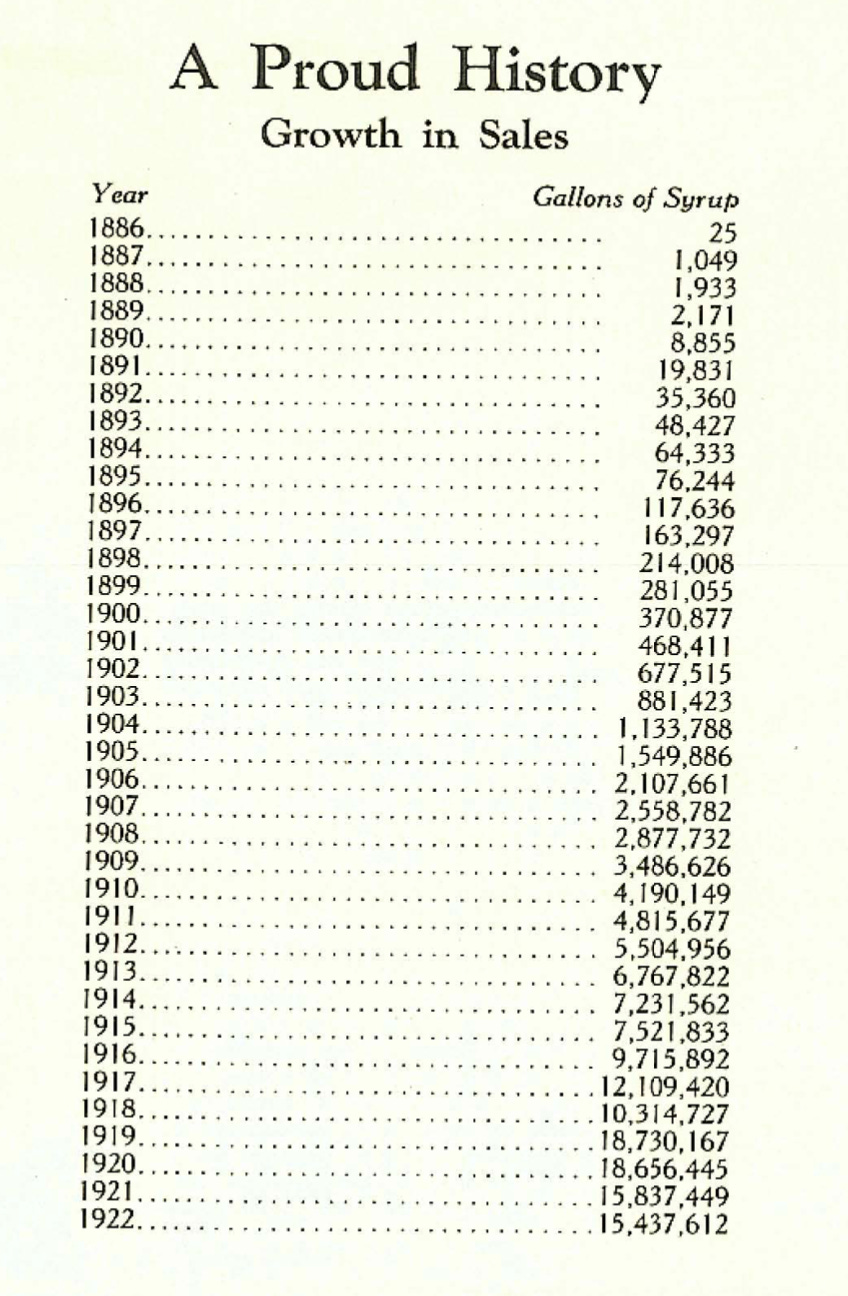

On February 26th, 1923, the Coca-Cola Company published its annual report for the fiscal year that just ended. The firm had quite a run since John Pemberton invented the Coca-Cola formula in 1886. Pemberton sold 25 gallons of Coke syrup in that inaugural year. In 1922, the company sold 15.4 million gallons. This had been incredible growth within the young soft drink industry that Coca-Cola had popularized.

Since the time Coke was invented until 1917, the company enjoyed growth in terms of gallons sold every single year. Despite this perfect 31 year streak of growth, sales volume appeared to slow down in the handful of years that followed. The number of gallons sold declined in 4 of the next 5 years. When I looked at this annual report recently, I thought about some questions that might have come to my mind in 1923 if I was an investor. Was this a trend that signaled a decline in the prospects of the Coca-Cola Company? Was the market saturated at this point in time? Was competition eroding the strength of this franchise? Would it be able to expand overseas into more international markets? Is management less motivated after selling control in the company? Maybe a little background on the company during this time period is needed…

Only a few years after Pemberton created Coca-Cola, he sold the business to Asa Candler. Coca-Cola experienced tremendous growth under the leadership of Candler, becoming a strong organization within the beverage industry. In 1919, Ernest Woodruff organized the acquisition of Coca-Cola from the Candler family. Woodruff was the President of the Trust Company of Georgia, which is now known as SunTrust after it merged with Sun Bank in the 1980’s. The bank helped underwrite a public offering for Coca-Cola at the time, receiving shares in the company as payment for its services. SunTrust owned this stake for many decades, turning $110,000 into a few billion dollars. The bank sold its Coke shares between 2007 and 2012 to be better aligned with the stress test and capital requirements from regulators at the Federal Reserve following the financial crisis.

Charles Candler, the son of Asa Candler, was the President of Coca-Cola in 1923 despite selling the company a few years earlier. Woodruff was on the Board of Directors as well as on the Executive Committee. If I was an investor in 1923, I might be wondering if management was less motivated after selling the company. The number of gallons sold decreased each year following the sale in 1919. In addition, how much sugar water did the world really need? It is nice to see a company with a history of growth, but I am cautious to just extrapolate a company’s historical growth rate out into infinity.

It turns out that there was a logical explanation for the decrease in gallons sold in 1918. The US enacted sugar rations that year due to World War One, and sugar is an important part of Coke’s syrup. Even back in that time period, Coca-Cola was the largest consumer of sugar in the world. After the war ended, the economy faced a brief recession as well. Maybe this explains the lack of growth in the early 1920’s for Coca-Cola. On the other hand, a decline in sales is inevitable at some point, as no business can grow every single year. This was a unique period of time for the business, which can make year over year comparisons difficult.

Was the total addressable market pretty tapped out at this point in time? The 1922 annual report showed the map below. Although the map looks pretty dense in the east, the western United States appears to be less saturated. The company had plants in the US, Canada, and Cuba at this point in time. Additionally, 1922 was the first year of operations of a plant in France. The 1922 annual report states that its products were also sold in “the Hawaiian islands, Puerto Rico, Panama, Mexico, Australia, New Zealand, England, France, and in the Orient”. The soda fountain was an American tradition, and it had been “ignored and taboo abroad”. The company thought that the international prospects were in the midst of changing for the better, but that was yet to be proven out.

Could new entrants emerge? Although the Coca-Cola Company famously kept its secret formula locked in a vault, the formula was not important to the value of the company. Keeping the formula secret was more of a marketing tactic. Dr. Pepper already existed before Coca-Cola, and other similar products would emerge. The real competitive advantages that Coca-Cola would develop over the ensuing decades were in terms of its brand and its distribution system. It was clear by reading its annual reports in the 1920’s that Coca-Cola understood the importance of these two items.

Coca-Cola’s brand has been developed through advertising over many decades. Generations of people have associated Coke with positive memories, whether consciously or unconsciously. You would be more likely to see images of Coca-Cola at a sporting event than at a funeral, for example. The company spent $11,402 on advertising all the way back in 1892, and consistently poured money into ads since that time. Although it hurt profitability when viewing an individual year, this money spent on advertising added up cumulatively to result in a strong brand for the company, giving it a competitive advantage that wouldn’t have existed without the investment.

Coca-Cola appears to have always taken its distribution seriously. In the 1923 annual report, shown in the image above, the company became concerned with bottlers who “allowed themselves to become discouraged and get into a state of lethargy”. While I’m not sure if lethargy really was to blame for a lack of sales volume, the distribution system of Coca-Cola was a crucial part of the company’s operations. In 1922, the distribution system consisted of 1,200 bottlers, 105,000 fountain dealers, and 150,000 bottle dealers. Due to a historical accident, as well as due to the fact that it reduced the capital expenditure burden, these bottlers and dealers were independent organizations outside of the Coca-Cola Company.

Once Coca-Cola’s distribution system was in place, it made it easier and more profitable to sell additional brands. The company has over 200 brands today, including different soda flavors, water, coffee, tea, and more. Additionally, the strong distribution system made Coke more available to the public. Availability increases brand recognition, but it also increases demand and can help to form habits among consumers. You’re more likely to eat an unhealthy snack if you walk by it and see it 10 times a day in your house versus if it was hidden on the top shelf in your kitchen.

Most importantly though, a larger and stronger distribution system made it more difficult for competitors to replicate it. The capital expenditure required for a company to recreate this distribution system internally would be massive. It wouldn’t be so simple to recreate it externally, either. Retailers only have so much shelf space, and if Coke is selling well then you don’t need that many other brands sitting next to it.

Obviously Coca-Cola has competitors today, so these competitive advantages don’t mean that competition would be zero. They just provide a moat that limits some amount of new entrants within the industry. Notice how most towns have a local microbrewery, but there aren’t many local soda brands. Richard Branson disrupted a few industries, but his Virgin Cola was unable to find success. Private label brands have done well for retailers in recent years, but that is the case less so in the soft drink industry than with other types of products.

Despite the decline in sales volume during this time period, there were reasons to be optimistic as well. The company was acquired for $25 million in 1919. Coke reported net income of $2.3 million in 1921, which was a yield of 9.4% based on Ernest Woodruff’s purchase price. This amounted to a return on assets of 6.6% and a return on equity of 7.4%. The return on capital figures don’t look great at first glance. However, ‘Formulae, Trademarks, and Goodwill’ made up 70% of assets. I assume this was the result of Woodruff’s acquisition of the company in 1919. Ignoring these intangible assets like goodwill, the return on net tangible assets for Coke would have amounted to an excellent 34.3% in 1921.

Despite the decrease in both revenue and gallons sold in 1922, net income grew to be $6.3 million that year. This amounted to a yield of 25% based on the 1919 acquisition price. The increase in profitability was the result of improved gross margins, as the cost of goods sold decreased from $21.2 million in 1921 to $9.7 million in 1922. There might have been some sort of accounting change in terms of revenue recognition at this time, since this is a major change in the gross margin. Even if that was the case, profitability still must have genuinely improved. It is unclear from the annual report exactly why this occurred though.

As the 1920’s roar on, it will be interesting to look back and see how the company performs. In particular, I plan to take a closer look at how its stock price reacted to the Great Depression. I wonder if the business performance diverged at all from what I presume was a decreasing valuation. My final takeaway from this time period is that I aspire to be like the Woodruff’s and SunTrust: be alert (or lucky enough) to find a great opportunity, and then be wise enough to hold it for a hundred years or so.